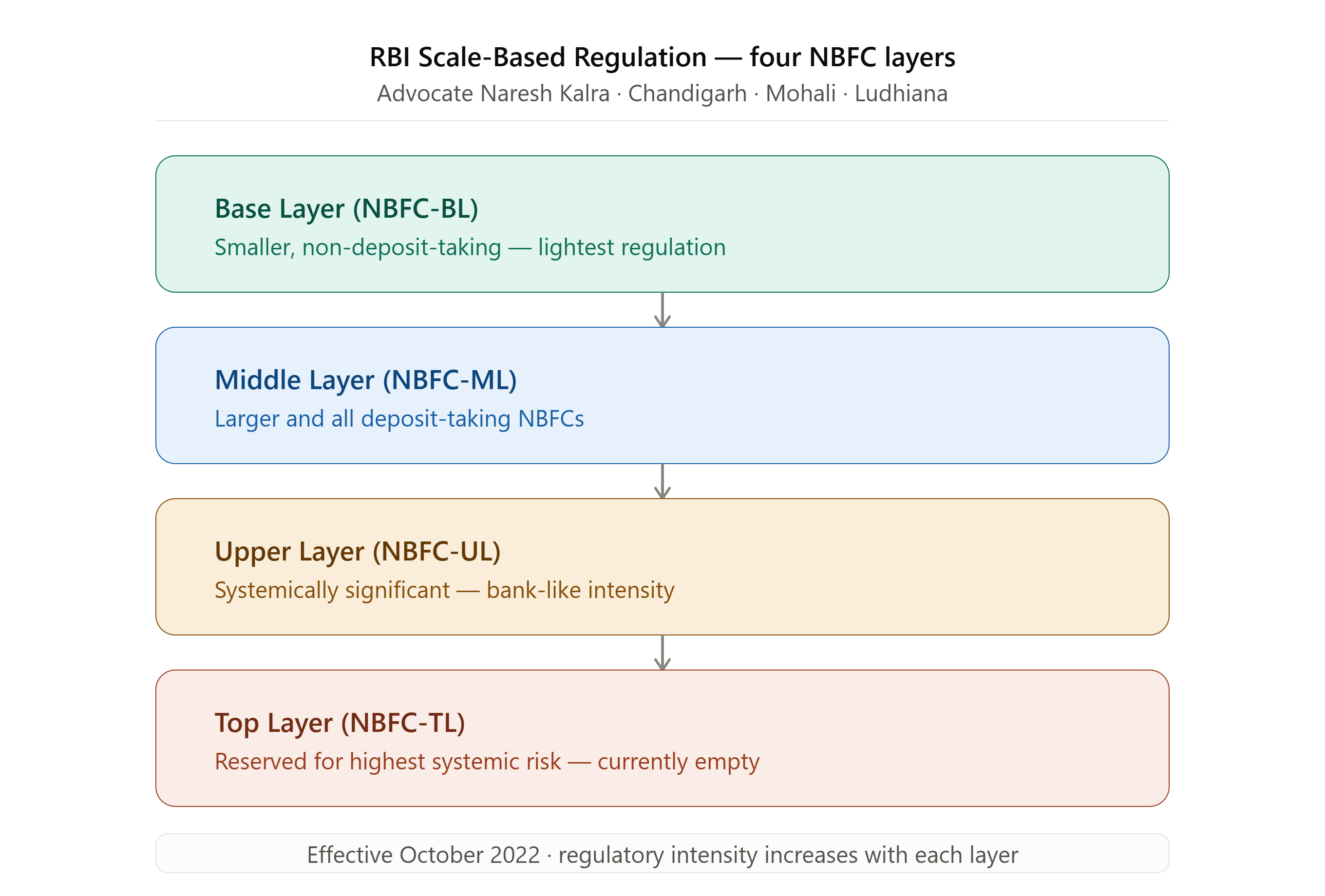

What is RBI's Scale-Based Regulation framework, and why does it matter for my NBFC?

Effective October 2022, RBI restructured NBFC regulation into four layers — Base, Middle, Upper, and Top — based on size, activity, and systemic risk, with escalating regulatory intensity at each layer. Understanding which layer your planned NBFC will occupy is essential before you even begin the registration process, since it determines your capital requirements, governance obligations, and ongoing compliance burden. Our NBFC Registration Lawyer India team in Chandigarh assesses this classification with you at the planning stage.

What is the minimum capital required to register an NBFC in India?

RBI has progressively increased minimum Net Owned Fund requirements for NBFC-Investment and Credit Companies under a phased schedule, and these figures are periodically revised by RBI circular. Rather than relying on a fixed figure that may be outdated, our NBFC Compliance Advocate India team in Chandigarh confirms the exact current threshold applicable to your specific category and SBR layer before you begin capital planning.

How is an NBFC different from a bank?

NBFCs cannot accept demand deposits (like savings or current accounts), cannot issue self-drawn cheques, are not part of the core payment settlement system, and their deposits (where accepted, for deposit-taking NBFCs) are not covered by deposit insurance the way bank deposits are. NBFCs generally face a comparatively lighter regulatory burden than fully licensed banks at the Base and Middle Layers, though Upper Layer NBFCs face increasingly bank-like regulatory intensity under the SBR framework.

How long does NBFC registration take in India?

Timeline varies considerably based on the completeness and quality of the initial application, the NBFC category, and RBI's clarification requests during scrutiny. Applications with precise documentation and a well-structured business plan generally move through the process significantly faster than incomplete filings that trigger repeated clarification rounds. Our NBFC Registration Lawyer India team in Chandigarh prepares applications specifically to minimize these delays.

What happens if my NBFC fails to maintain compliance after registration?

Non-compliance with NOF maintenance, Capital Adequacy Ratio requirements, periodic filing obligations, or RBI's Fair Practices Code can result in penalties, business restrictions, or in serious cases, cancellation of the Certificate of Registration. The severity of consequences and intensity of oversight scale with your NBFC's SBR layer. Our NBFC Compliance Advocate India team in Chandigarh and Ludhiana provides ongoing compliance support to help NBFCs avoid these outcomes.